Group 1 Automotive: Strong Performance Is Being Ignored (NYSE:GPI)

Apriori1/iStock via Getty Images

Beyond any doubt, one of the most attractive investment opportunities on the market today is Group 1 Automotive (NYSE:GPI). Although investors might be concerned, and rightfully so, about what will happen to automotive demand in the event that we do go into a recession, the company has demonstrated a fantastic propensity for growth. In addition to growing organically, the company continues to grow by means of acquisition. Shares of the business also look incredibly cheap on both an absolute basis and relative to similar firms. Even if financial performance were to revert back to what it was in prior years, the company would still look very affordable. Because of this, I’ve decided to retain my ‘strong buy’ rating for the company.

Still growing nicely

Back on March 11th of this year, I wrote an article about Group 1 Automotive wherein I said that the company still makes for a strong prospect for investors. I cited the company’s strong revenue growth and robust cash flows. I also said that shares were incredibly cheap at that time. This led me to retain my ‘strong buy’ rating for the business. Since then, things have been a bit difficult. At present, shares have generated a loss for investors since that article was published in the amount of 11.7%. Although this is painful, it is better than the 14.1% decline experienced by the S&P 500 during the same timeframe.

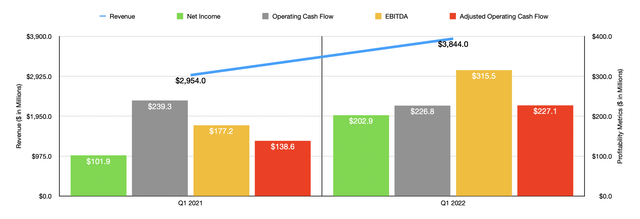

At first glance, investors may think that the reason for this decline in price may have to do with weak fundamental performance achieved by the company. However, it really is just a case of the broader market being fearful of what the future holds. When you dig into the fundamental performance of the company since then, which really only covers the first quarter of its 2022 fiscal year, the results are promising. Management reported revenue for that quarter of $3.84 billion. That represents an increase of 30.1% compared to the $2.95 billion reported the same time one year earlier.

Author – SEC EDGAR Data

The year-over-year improvement for the company came as all revenue categories showed attractive growth. New vehicle retail sales increased by 15.6%, while used vehicle retail sales jumped by 53.1%. On the used vehicle wholesale side, revenue rose by 19.5%. Parts and service sales also continue to decline year over year, jumping by 34%, while the finance and insurance side of the company expanded by 37.7%. There is a lot to unpack here though. For starters, the average sales price of a new unit sold increased by 12.4%, climbing from $42,285 to $47,509. The increase for used vehicle retail sales was even greater, jumping by 31.2% from $23,656 to $31,043. The company did benefit from a combination of acquisitions and same-store sales increases. Total revenue on a same-store basis increased by 11%, with every category except for new vehicle retail sales increasing. Under the new vehicle retail sales category, revenue dropped by 3.3% as the number of retail new vehicles sold dropped by 14.2%.

Acquisitions for the company also helped to push revenue higher. The most notable of these was of Prime Automotive Group. Management acquired this company In November of 2021 in a deal that included 28 dealerships, other related real estate, and three collision centers. The total price for the deal was $934.2 million. However, certain adjustments pushed this up to $967.6 million. The company also purchased some other assets recently, including a Toyota dealership that cost the company $250.4 million and, last year, two Toyota dealerships for a combined $49.9 million.

As revenue has risen, so too has profitability. Net income in the first quarter, for instance, came in at $202.9 million. That’s nearly double the $101.9 million reported the same time one year earlier. Other profitability metrics have also followed suit. Although operating cash flow for the company did decline year over year, dropping from $239.3 million to $226.8 million, it would have actually increased from $138.6 million to $227.1 million if we ignore changes in working capital. Meanwhile, EBITDA also improved, climbing from $177.2 million to $315.5 million. In light of this profitability, the company has also made some other interesting moves. For instance, it recently announced that it was increasing its share buyback program by $175 million, taking it up to $250 million in all. This follows $143.1 million worth of share repurchases so far this year, representing 4.1% of the company’s stock outstanding. In addition to this, the company also announced the acquisition, on April 4th of this year, of another Toyota property in New Mexico that will bring $115 million in annual revenue to the business. Terms were not disclosed, but the company did say that total revenue, on an annualized basis, brought on to the company as a result of acquisitions this year has now risen to $550 million. In all, this increases the company’s auto dealership count to 202 locations.

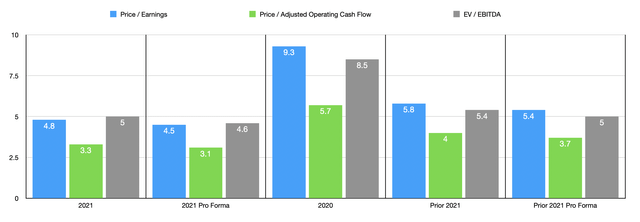

No real guidance was given for how the company would perform for 2022 as a whole. So instead, I decided to value the business based on 2021 results. Doing so, we see that the company is trading at a price-to-earnings multiple of 4.8. However, in its annual report for 2021, the company provided estimates of what revenue and profitability would look like if all of the acquisitions it made last year were part of the business at the beginning of 2021. That would bring the price to earnings multiple for the company down to just 4.5. The price to adjusted operating cash flow multiple is even lower at 3.3, a number that drops to 3.1 if we rely on my own 2021 pro forma estimates. Using this same approach, the EV to EBITDA multiple for the company should drop from 5 to 4.6.

Author – SEC EDGAR Data

As you can see in the table above, all of this pricing looks even better than when I last wrote about the company. In addition to that, I also calculated how shares are priced if we saw financial performance revert back to what it was in 2020. Even in this case, the company does not look particularly pricey, with a price to earnings multiple of 9.3, a price to adjusted operating cash flow multiple of 5.7, and an EV to EBITDA multiple of 8.5. To put this all in perspective, I decided to compare the company’s 2021 results, not the pro forma ones, to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 4.5 to a high of 11.5. Meanwhile, using the EV to EBITDA approach, the range was from 4.7 to 7.2. In both cases, only one of the five companies was cheaper than Group 1 Automotive. Meanwhile, using the price to operating cash flow approach, the range was from 4.4 to 6.7. In this case, our prospect was the cheapest of the group.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Group 1 Automotive | 4.8 | 3.3 | 5.0 |

| Sonic Automotive (SAH) | 4.5 | 5.2 | 6.3 |

| Lithia Motors (LAD) | 6.4 | 6.1 | 6.2 |

| AutoNation (AN) | 5.1 | 4.4 | 4.7 |

| Penske Automotive (PAG) | 6.1 | 5.8 | 5.7 |

| Murphy USA (MUSA) | 11.5 | 6.7 | 7.2 |

Takeaway

Right now, Group 1 Automotive is one of the most attractive opportunities on the market in my opinion. Although investors have taken a hit recently, the company continues to generate strong fundamental performance and I suspect that the long-term picture for the company is favorable. Given how cheap shares are, I have even gone so far as to make it the second-largest holding, as of this writing, in my portfolio. Because of how I have averaged down, I’m currently only down by 2.8%. But I fully suspect that the future for the business will be bright. And as such, I’ve decided to retain my ‘strong buy’ rating for the company.